You are 52. The mortgage is mostly handled. The kids are launching or close to it. On paper you are doing fine, and that is exactly the strange part. Because every guide you open about life planning in your 50s is really a retirement calculator in disguise. Run the numbers, max the 401(k), pick a portfolio, see you at 65. You came looking for a plan for the decade you are actually standing in, and someone handed you a spreadsheet about the decade after it.

That is the quiet frustration. You have the experience. You know how to plan a project, run a budget, manage a team. But planning your own next ten to fifteen years feels different, and weirdly harder, because nobody talks about the part where you are still here, still active, still building, for a long stretch before any of the retirement stuff matters.

You are not behind. You are at the part most advice skips.

What Life Planning in Your 50s Actually Means

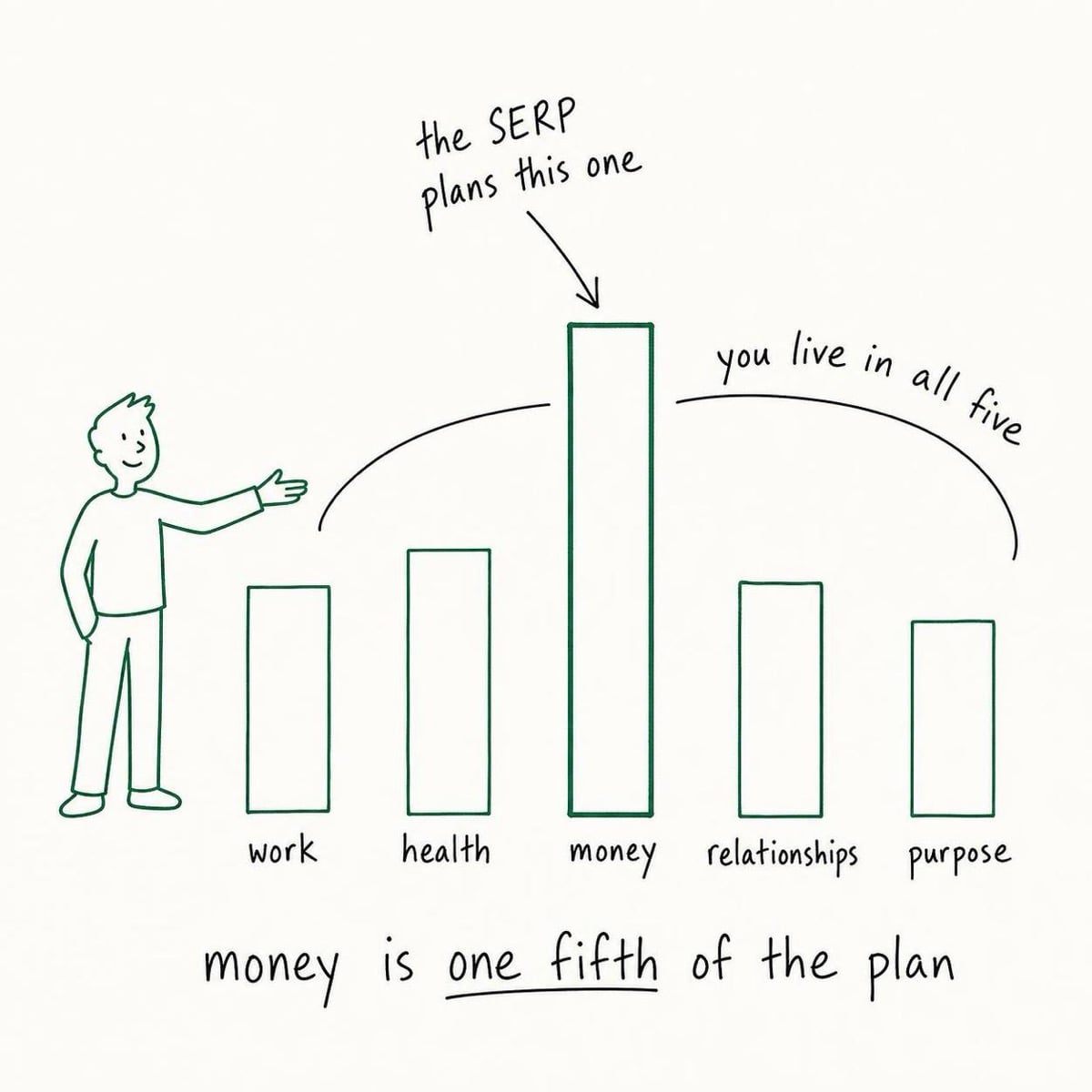

Life planning in your 50s means designing the next ten to fifteen active years across five domains, not just funding the years after them. The five are work, health, money, relationships, and purpose. Money is one of them, not the whole plan. At 50 you have, on average, another 25 to 35 years of life ahead, and a long stretch of it is active and capable, so the question is not only "can I afford to stop" but "what am I building while I am still going strong." [1]

The SERP for this query is almost entirely financial. Fidelity wants to model your cash flow. AARP has eight money moves. A certified planner walks you through withdrawal rates on YouTube. None of that is wrong. But it answers a narrower question than the one you are asking, because retirement planning in your 50s is a subset of life planning in your 50s, not a synonym for it. You can be financially set and still walk into your 60s with no plan for your body, your relationships, or what you actually do with your days. Plenty of people do. That gap is what this is about.

Why Most "50s Planning" Advice Misses the Point

Most 50s planning advice misses because it treats money as the whole problem and the 60s as the whole destination. The real risk in this decade is not just an underfunded account, it is an unbuilt life: a strong portfolio attached to a weak body, a thin set of friendships, and no answer to "what is this all for." Financial planners see this directly. In one 2025 survey, 89% of planners said their clients were not emotionally prepared for retirement even when the money was ready. [2]

Here is the part the calculators cannot price. Satisfaction with your relationships at 50 predicts your physical health at 80 better than your cholesterol does, according to the Harvard Study of Adult Development, which has tracked the same people for more than 80 years. [3] Money buys you options. It does not buy you the relationships, the health, or the sense of mattering that decide whether those options feel like anything. If your whole plan is the account balance, you have planned one domain and called it a life. This is the difference between a real life plan and a retirement number.

The Reframe: Plan the Runway, Not the Landing

Stop planning for the day you stop. Plan the runway you are walking right now. Life planning in your 50s is about the 50-to-65 stretch you are inside of, an active, capable decade and a half, not the 65-plus endpoint the SERP fixates on. This decade is when you still have the energy to change your body, deepen the friendships, switch the work, and decide what the rest is for. Treat your 50s as a setup phase and you waste the highest-return years you have left, spending them rehearsing for a finish line instead of building.

The research backs this stance hard. How much active, disease-free life you get is not fixed at 50, it is being decided by what you do in this decade. Women at 50 with four or five healthy lifestyle factors got 34.4 disease-free years ahead of them. Those with none got 23.7. That is a ten-year gap, and it is purchased with habits, not genes. [4]

Psychologists have understood midlife this way for decades. Daniel Levinson described middle adulthood as the stretch where you reappraise the commitments you made young, express the parts of yourself you shelved, and reconcile the gap between the early dream and the actual life, across work, family, and relationships at once. [5] That is not a crisis. It is a planning window. If you have been feeling stuck in your career or quietly restless about the shape of your days, that restlessness is the signal that the runway needs a plan, not that something is wrong with you.

A Five-Domain Plan You Can Actually Run

A workable plan for your 50s covers five domains and rebuilds them one at a time, not all at once. The domains are work, health, money, relationships, and purpose. The mistake is trying to overhaul all five in a January burst, which collapses by March. The method that holds is sequencing: pick the one domain that needs it most this quarter, get a single keystone habit running there, then let that win fund the next domain. Calm discipline over a ten-year horizon beats a frantic sprint that flames out.

Run each domain through the same three questions. Where is it now. Where do you want it by 60. What is the one small thing that moves it. Then plan only the first domain in detail this quarter.

Work. You may have ten to fifteen working years left, which is a long time to spend in a role you have outgrown. This is the decade for the deliberate move, not the panicked one: the career change at 50 made on purpose, the consulting shingle, the shift from climbing to contributing. People plan retirement obsessively and the work between now and then almost not at all. Plan the work.

Health. This is the domain with the highest return and the one most people defer. Your 50s body responds: light activity adds about 2.8 years to lifespan, moderate adds 4.5, and yes, you can build real muscle in your 40s and 50s. [6] Even modest, combined improvements in sleep, movement, and diet are tied to over a year of added lifespan and four-plus extra years of disease-free life. [7] Start with one habit, like a daily walk or fixing your sleep, and let it compound. The longevity math is unusually generous in this decade, and the longevity habits worth building now are mostly small and boring.

Money. Yes, this matters, and it is one fifth of the plan, not the whole thing. The catch-up window is real: if you are 50 with little saved, you still have a runway, and the move is consistent contributions plus better money habits you actually keep, not a heroic late bet. If you want to understand the vehicles before you commit, learn how investing actually works rather than chasing the "best portfolio for a 50-year-old" headline. The honest answer to "how much do I need" depends on your spending, not a magic number, and we cover that below.

Relationships. This is the domain the spreadsheets cannot model and the one that most decides how the next 30 years feel. Social isolation raises dementia risk by about 50% and heart disease and stroke risk by about 30%, independent of your finances. [8] Your 50s, with work demands easing and kids leaving, is when many people let friendships quietly thin out. Plan against that. Schedule the standing dinner. Learn how to make friends as an adult again, on purpose, because it does not happen by accident at this age.

Purpose. What is the work, the contribution, the thing that gets you up once the title and the kids are no longer doing it. Stanford's Center on Longevity proposes planning a "purpose portfolio" alongside the financial one, treating relationships, health, contribution, and meaning as assets you fund on purpose. [9] Multi-domain engagement across exactly these areas predicts how well people adjust later far better than any single domain does, and sustained engagement across them is tied to lower mortality. [10]

Do not start all five. Start one. The one that is hurting most right now.

What This Looks Like for a Real Person

Here is the five-domain plan running in an actual life. Marco is 54, an operations manager whose company just got acquired. His instinct was to do what the search results told him: open three retirement tabs and stress over whether his number was big enough. The number was fine. His life was not.

So he ran the five-domain pass on a Sunday with a coffee and one sheet of paper. Work: solid but stale, no plan past "keep doing this." Health: 22 pounds up since 45, sleep wrecked. Money: actually in decent shape. Relationships: two close friends he had not seen in a year. Purpose: a blank.

He did not fix all five. He picked the one bleeding worst, which was health, and ignored the rest for the quarter. One keystone habit: a 15-minute walk after his morning coffee, with a two-minute floor version for brutal days. That is it. By week eight it was automatic, the thing he did without arguing with himself.

Only then did he add domain two: relationships. One text to one old friend every Sunday, anchored to the same coffee. A standing monthly dinner on the calendar. Still nothing on work or purpose yet, on purpose.

By month nine, with health and friendships holding, he opened the work question without panic, the way you can only when you are not in crisis. A year in, Marco is not a man who "got disciplined." He is a man running a sequenced plan for a decade he used to treat as a waiting room. That is what planning for the next stretch looks like up close, the same calm method that lets people change their life at 60 and beyond: one domain at a time, in the right order, no heroics.

But I Am 50 With Almost Nothing Saved

That fear is real, and it is also the exact trap this whole reframe is built to spring you from. Being behind on money does not mean you are behind on life, and it definitely does not mean money is the only thing to plan. A late start on savings is a problem you can work on with consistent contributions and lower expenses over a real fifteen-year runway. Tying your entire self-worth to the account balance is a different problem, and a worse one, because it leaves the four domains that actually decide your wellbeing completely unplanned.

The honest position: money matters and it is fixable, and it is still one fifth of the plan. The Stanford longevity work and the Harvard study both land on the same uncomfortable point. People with strong relationships and a clear sense of purpose show markedly lower mortality and better health regardless of where their portfolio sits. [11] Plan the money. Then plan the rest, because the rest is what the money was supposed to protect. If this stretch has felt more like a midlife crisis than a plan, the move is the same: stop trying to fix everything at once and rebuild one domain at a time.

The One Thing to Do This Week

Take a single sheet of paper. Write five words down the side: work, health, money, relationships, purpose. For each, write one line on where it stands right now, honestly. Then circle the one that is hurting most, the domain you would least want to read out loud. That circle is your starting point for life planning in your 50s, and the only one you plan in detail this quarter.

Pick one small keystone habit inside that single domain. Anchor it to something you already do every day. Leave the other four alone for now. They get their turn, in order, as each prior win starts holding on its own.

You have the experience to plan a decade. You have just never been handed a frame that treats your 50s as years to live rather than years to fund. You are not at the landing. You are on the runway, and it is longer and more open than the spreadsheets let on.