The 401(k) statement has been sitting in your inbox for three weeks, unopened. You know the drill: you click it, see a balance that feels too small for someone your age, get a small drop in your stomach, and close the tab. So you don't click. You earn more than you ever have, you can run a household budget in your head, and you still have no clean answer to a simple question: are you actually okay, money-wise? Years of that, and it has become the system: avoid, feel vaguely behind, repeat.

Figuring out how to get your finances in order in your 40s has nothing to do with willpower you can't seem to find. You run budgets at work. You manage a household. You are not financially illiterate. What's missing is a fixed order of operations for your money, the same kind of sequence your job and your kids' schedule already have. Without it, money stays in the "I'll deal with it" pile, next to the other parts of life that keep slipping while you handle whatever is on fire today.

Right now your money runs on willpower. In this decade, with retirement finally in view, it needs to run on a system instead.

Where Should a 40-Year-Old Be Financially

A 40-year-old is "on track" with roughly three times their annual salary saved for retirement (Fidelity's benchmark), three to six months of expenses in an emergency fund, and high-interest debt under control. But most people aren't there, and that is normal, not a verdict. The median 40-year-old holds about $37,700 in financial assets outside home equity, and nearly 40% of Americans in their 40s have no retirement savings at all. [1]

So if you feel behind, you have a lot of company. The benchmark is a target, not a scoreboard you've already lost. And here's the part that matters more than the number: your 40s are peak earning years, and compound interest still has 20 to 25 years of runway before retirement, which makes catch-up saving in this decade pay off far more than it will later. That runway is also why it pays to start treating retirement saving as something you can still catch up on rather than a verdict that's already in.

The math is blunt. Starting at 40, saving about $15,000 a year reaches a $1M target by 65 at a 7% return. Wait until 50 and you need nearly $37,500 a year to hit the same number. [2] That's the whole reason financial planning in your 40s feels urgent in a way it didn't at 30. The cost of waiting just got steep. The window is still wide open.

Why "Getting Organized" Keeps Failing You

Getting your finances in order keeps failing because you treat money as one giant chaotic project instead of a short sequence of small, ordered moves. Faced with a tangle of accounts, debts, retirement decisions, and college worries, the brain does what brains do under overwhelm: it picks the easy default, which is to close the tab. The fix is not a marathon budgeting session. It's deciding the order once, automating the first step, and never having to summon willpower again.

There's research behind that avoidance. Under stress and overload, people lean on inertia and the status quo, which is exactly why most folks never change a default once it's set. Behavioral economists Benartzi and Thaler showed this is a two-way street: inertia keeps people stuck, but it also becomes a powerful tool the moment a good default is in place, like automatic enrollment in a retirement plan. [3]

This is the same trap that shows up everywhere else in midlife. The routine you meant to keep, the health habit you abandoned, the money check you postponed: all of it dies the same way, postponed to a calmer week that never comes. We've written about that pattern in the broader midlife reset, and money is just the domain people avoid the longest because the numbers feel like a judgment. Part of the fix is loosening the money mindset that treats every statement as a report card, so opening the tab stops feeling like a verdict.

So stop trying to "get organized" through effort. Effort is the thing that runs out. What survives a chaotic month is structure that runs without you.

The Order of Operations That Actually Works

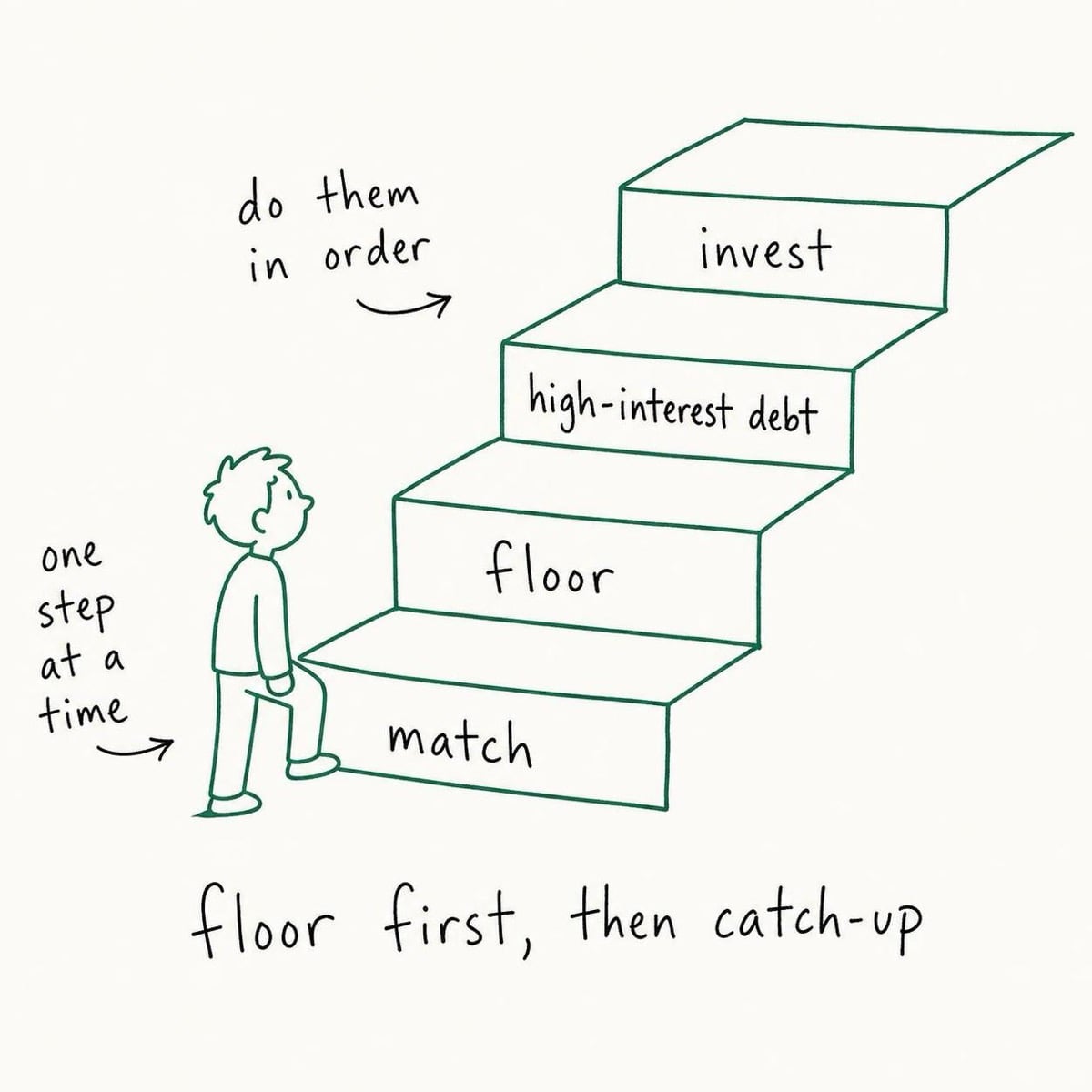

The reframe that fixes your finances in your 40s: there is a correct order for every spare dollar, and following it beats budgeting harder. You don't need to optimize everything at once. You need to know which dollar goes where first. Vanguard's framework ranks it cleanly: capture the full employer 401(k) match (the highest guaranteed return you'll ever get), build a starter emergency fund, kill high-interest debt, then put more toward retirement. [4]

Walk through it in plain terms, because the order is the whole point.

First, grab the match. If your employer matches 401(k) contributions and you're not contributing enough to get all of it, you are turning down a 50% to 100% instant return. Nothing else on this list beats that. [5] This is the single best-returning move in retirement planning in your 40s, and it takes one form and ten minutes.

Second, build the floor. A small emergency fund is the floor method applied to money: a few thousand dollars in a separate account, enough to absorb a surprise without reaching for a credit card. Set the minimum that lets you breathe, then stop optimizing it. Vanguard found that holding just $2,000 in emergency savings raised people's financial well-being by 21%, with another 13% gain once they reached three to six months of expenses. [6] The calm you're after has a price tag, and it's surprisingly small.

Third, kill high-interest debt. Anything above roughly 20% APR (most credit cards) gets attacked next, because no investment reliably beats that rate. Paying off a 22% balance is a guaranteed 22% return. [5]

Fourth, feed retirement. Now you push past the match into the rest of your retirement savings and longer-term investing. By your 40s you also get IRS catch-up room, the extra contribution limits that exist precisely for this decade.

This sequence is why we keep saying: rebuild one system at a time, in the right order. Money is not different from the rest of the rebuild. It just needs its own queue. That is the real answer to how to get your finances in order in your 40s: not more effort, a settled order. If the investing piece is where you stall, the basics of how to invest without overthinking it clear most of the fog, and the day-to-day side is just better money habits running on a schedule.

What This Looks Like on a Real Month

Here's the order of operations as a lived month, not a theory. Marco is 47, an operations manager, married, two kids, a car loan, a credit card balance he's been "meaning to deal with," and a 401(k) he contributes 3% to without knowing his employer matches up to 5%. He earns well. He still feels behind every time the topic comes up, which is why the topic rarely comes up.

He doesn't budget harder. He runs the sequence once.

Saturday morning, coffee in hand, he does step one: bumps his 401(k) from 3% to 5% to capture the full match. Ten minutes, online, done. That single move is free money he was leaving on the table every paycheck. Step two, he opens a separate high-yield savings account and sets a $200 automatic transfer for the day after payday, building toward a starter emergency fund. He doesn't have to remember it or feel motivated. The transfer happens whether or not it's a good week. That's the entire trick: automation beats willpower, the same way an anchored cue beats a good mood when you're trying to stay consistent with any goal.

The credit card is next in the queue, not today. He lists the balance and the rate, points his extra cash at it after the match and the starter floor, and leaves the car loan alone because its rate is low. He doesn't touch investing strategy yet. One queue, in order. No spreadsheet color-coding, no app with 40 categories, no Sunday-night dread. Three decisions, two of them automated, and the fourth one parked until the third is done.

This is also how the Save More Tomorrow program got ordinary workers from a 3.5% savings rate to 13.6% over 40 months: not by demanding discipline, but by tying savings increases to future raises and letting inertia do the work. Once enrolled, 80% stayed in through four or more pay raises. [7] Marco copies the idea: he sets his 401(k) to auto-escalate 1% every year. He'll be saving far more in five years and will barely feel it.

A year in, Marco isn't a more disciplined person. He's the same person running a money system that doesn't ask him to be disciplined.

The Quick-Math Rules, Decoded

Those money "rules" floating around (the $27.40 rule, the 3-6-9 rule, the $1,000-a-month rule) are mental shortcuts, not laws. They're useful as rough targets to anchor a vague goal, and useless if they replace the order of operations above. The $27.40 rule says saving $27.40 a day equals $10,000 a year, a way to shrink a big annual goal into a daily one. The $1,000-a-month rule estimates you need about $240,000 saved for every $1,000 of monthly retirement income you want, at a 5% withdrawal rate.

The 3-6-9 rule is the handiest for building the floor we just covered: aim for 3 months of expenses saved first, then 6, then 9 as your emergency cushion grows. It turns "save more" into three concrete checkpoints. Treat all of these as budgeting tips for your 40s that make abstract financial goals feel reachable, not as a strategy by themselves. The strategy is the sequence. The rules are just friendlier ways to size each step.

Money management in your 40s gets easier when you stop chasing the perfect rule and start running a good-enough one on autopilot. A rough plan you actually follow beats a perfect plan you avoid. That's true for money, and it's the same truth behind any durable daily routine: the system you keep wins over the system you admire.

But You've Tried to Fix Your Finances Before

Fair. Most people have started a budget, tracked spending for two weeks, and quit. The usual reason isn't weakness. It's that you tried to fix everything at once through manual effort, which is the same overwhelm in a spreadsheet. The order of operations works differently: you make a handful of one-time decisions, automate them, and stop relying on monthly motivation that was always going to fade.

The other objection is time, and money rewards the impatient here. You don't need a weekend. You need the next 30 minutes to do exactly one thing: capture your employer match. That's the highest-return move on the entire list, and it's a single form. Everything else can wait for next Saturday.

And the "my situation is more complicated" objection usually isn't, at least not for the first three steps. A messier balance sheet (a side business, a second mortgage, an old 401(k) from a job two employers ago) changes the later optimization, not the order you start in. Match, floor, high-interest debt: that sequence holds whether your finances are simple or tangled. The complexity lives downstream, after the basics are running. This same "shrink it, automate it, sequence it" logic is what makes a financial checklist for your 40s something you finish instead of something you flinch at, and it plugs straight into making a life plan that treats money as one domain among work, health, and family rather than a separate crisis.

Start With One Move This Week

Open your retirement account today and check one number: are you contributing enough to get your full employer match? If not, raise it until you are. That's the single highest-return financial decision available to you, and it takes about ten minutes. Then pick the next item in the queue (a small automatic transfer to a starter emergency fund) and schedule it for the day after your next paycheck.

That's how to get your finances in order in your 40s without a budgeting overhaul or a personality change. Not 20 hacks. One ordered sequence, automated step by step, running quietly under a busy life. Money becomes one calm system instead of the thing you keep avoiding, and it sits next to the rest of your rebuild instead of separate from it. Capture the match this week, and every quiet paycheck after that does the compounding you've been putting off.