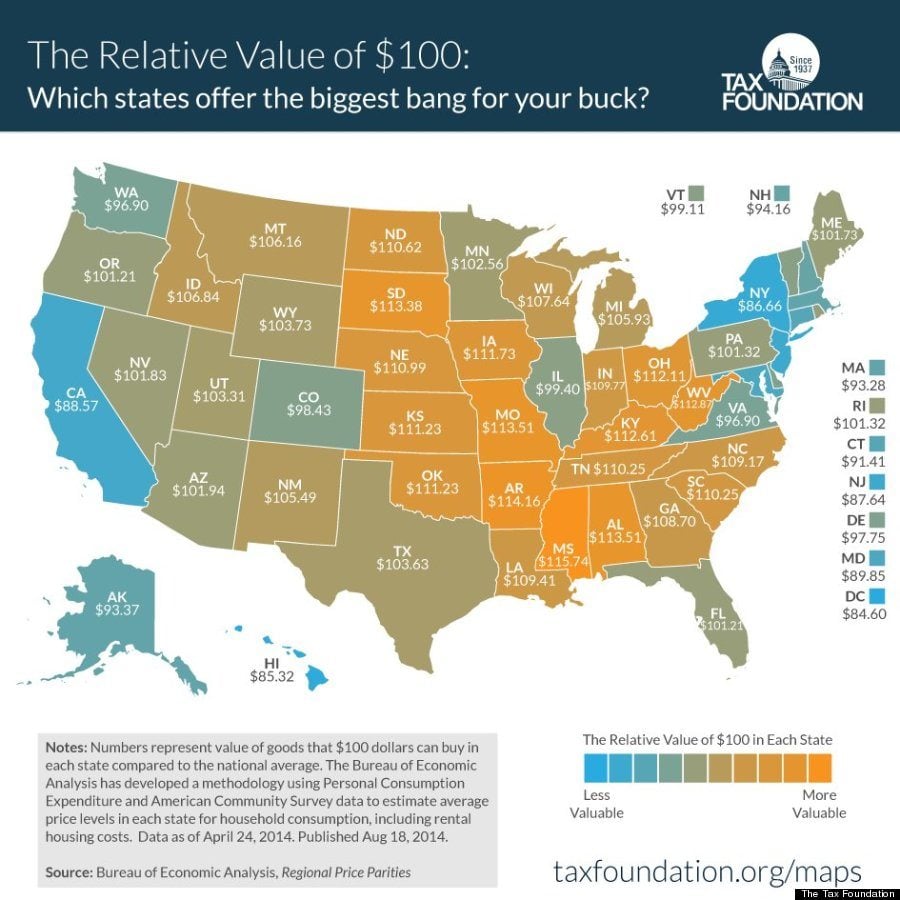

2017 cost-of-living index figures by C2ER (Council for Community and Economic Research) are fresh out of the oven. Well, despite continued widespread recovery tactics, where you live in America has a great deal of impact on what economic challenges you face. No country is immune from economic slumps but higher than average state autonomy in America means economic growth varies by state. While one might expect to see California and New York on the list of most expensive states in America, shifting economic landscapes make several unexpected states more expensive as well. Complicated economic factors, as well as public officials struggling to meet the challenges of the future, make these ten states the most expensive and most affordable in America.

Take palm-fringed, sandy beaches, sizzling cultural melt, and add incredibly beautiful flora and fauna - and that’s the ‘magical’ allure of Hawaii. All these goodies, however, come with a steep price. Looking to buy a home in Hawaii? That’ll set you back a whopping $1 million on average. And that isn’t all - it’ll cost you nearly$3000 to rent a two-bedroom apartment and the monthly energy bill is estimated at $455.51, a figure that’s about 3 times what you’d shed in some leafy suburbs of California. But you live in Hawaii, the Aloha State!

2. New York

Chiming at the second place is the Empire State. That in and of itself isn’t surprising at all in a state where the average home goes for $1.6 million (yes, you read that right). Looking to rent? Forget about it; a cozy two-bedroom apartment averages $4200 in monthly rent. Of course, New York is vast and uneven recovery/growth is partly to blame. Despite the improvement in unemployment rates since the end recession, New York continues to battle with aging infrastructure and starkly different growth rates. But there are areas like Rochester (average home price is $287000) where life is surprisingly easier than Manhattan. Nonetheless, you will still shed more than $160 for monthly energy bill there.

3. California

Not surprisingly, California is also one of the most expensive states in America. High housing costs in this state have long made it one of the pricier states, but population growth is another concern. At around $1 million, the average price of a home in metro San Francisco is the 3rd highest nationwide. California is also the number one state for poverty, reportedly carrying $1.6 billion in debt. While the state holds only 12% of the American population, nearly 33% of all welfare recipients are Californian.

4. Massachusetts

It’s official - it’s now more expensive to live in Massachusetts than Alaska! The cost of groceries is through the roof, with 24-ounce T-bone steak going for more than $62! While the average price of a home is $634,233, expect to pay 3 or even 5 more times in most Newton, Framingham, and Cambridge neighborhoods. At $2668, the average rent for a sweet two-bedroom apartment in Boston is the 4th highest in the US. And the energy bill of $287.63 is close to $100 more than would be in Anchorage.

5. Alaska

A newcomer to this list, Alaska – the moose state – offers unsurpassed natural beauty and close-knit culture you’ll never find elsewhere. With only 760 farms, it’s no surprise that most produce and food items are hauled from different states. And that trickles down to tons of other costs. A loaf of bread which goes for a mere $1.79 in Iowa will set you back $4.68 in Anchorage. But again, this is Alaska – the land of amazing wildlife. Paying utility bills ($201.39 for energy) and healthcare isn’t a walk in the park either.

One of the less densely populated states, Mississippi is one of the least expensive states to live in. With low per capita income, the state’s housing costs remain correspondingly low as well (the average home price of $199,028), making the cost of living affordable. Mississippi previously relied mainly on cotton production to drive the economy. In the last two decades or so, however, Mississippi has diversified agricultural and livestock industries, ensuring economic growth. Now focusing on producing rice, soybeans, chicken, and catfish, Mississippi continues to pursue diversification to enrich its economy, a strategy which has been successful so far.

2. Indiana

Next up, is Indiana, a state famous for the Indianapolis 500 and low-cost homes (averaged at $270,204). At the Crossroads of America, you can expect rock-bottom prices for groceries and other basic food items. A head of lettuce goes for a paltry $1.04 while a pound of coffee and ground beef will set you back just $4.43 and $3.74 respectively. A boom in the local economy has pushed prices up a teensy bit, but you can still pick up a check at dinner.

3. Michigan

The Great Lakes State, much like Mississippi and Arkansas, offer low-cost housing (averaged at $274,355) for consumers, yet it’s consistently ranked in the top ten for best states to do business. After all, this is the home of the American auto industry. The average gas price in Detroit was about $2.04 when it hit more than $3 in most parts of the country. The auto industry has bounced back, healthcare is thriving and high-tech jobs are supplanting manufacturing, helping this state become more competitive to prospective employers, keeping the economy working for Michigan citizens.

4. Arkansas

Like Mississippi, Arkansas is a more rural state, offering consumers low housing costs. Arkansas also boasts incredibly low costs for doing business, attracting six Fortune 500 companies to the state. Rent for a two-bedroom apartment is just $700 a month and the monthly energy bill is $145.79, roughly half of what you’d pay in Massachusetts. In short, Arkansas’ low cost of living is balanced by a lower household income than average but still remains a top state for the economic climate.

5. Oklahoma

Rounding up our list is the Sooner State, the home of undulating wheat fields. And the cost of groceries, including a loaf of wheat bread for less than $3, is appropriately cheap. Well, that isn’t all – a grand 2,400 square-foot home will only chip off around $300K from your bank account. With a sub-$150 monthly energy bill and low-cost health care, Oklahoma is certainly one of the best places you’d be lucky to call home.

Most Expensive States

1. HawaiiTake palm-fringed, sandy beaches, sizzling cultural melt, and add incredibly beautiful flora and fauna - and that’s the ‘magical’ allure of Hawaii. All these goodies, however, come with a steep price. Looking to buy a home in Hawaii? That’ll set you back a whopping $1 million on average. And that isn’t all - it’ll cost you nearly$3000 to rent a two-bedroom apartment and the monthly energy bill is estimated at $455.51, a figure that’s about 3 times what you’d shed in some leafy suburbs of California. But you live in Hawaii, the Aloha State!

2. New York

Chiming at the second place is the Empire State. That in and of itself isn’t surprising at all in a state where the average home goes for $1.6 million (yes, you read that right). Looking to rent? Forget about it; a cozy two-bedroom apartment averages $4200 in monthly rent. Of course, New York is vast and uneven recovery/growth is partly to blame. Despite the improvement in unemployment rates since the end recession, New York continues to battle with aging infrastructure and starkly different growth rates. But there are areas like Rochester (average home price is $287000) where life is surprisingly easier than Manhattan. Nonetheless, you will still shed more than $160 for monthly energy bill there.

3. California

Not surprisingly, California is also one of the most expensive states in America. High housing costs in this state have long made it one of the pricier states, but population growth is another concern. At around $1 million, the average price of a home in metro San Francisco is the 3rd highest nationwide. California is also the number one state for poverty, reportedly carrying $1.6 billion in debt. While the state holds only 12% of the American population, nearly 33% of all welfare recipients are Californian.

4. Massachusetts

It’s official - it’s now more expensive to live in Massachusetts than Alaska! The cost of groceries is through the roof, with 24-ounce T-bone steak going for more than $62! While the average price of a home is $634,233, expect to pay 3 or even 5 more times in most Newton, Framingham, and Cambridge neighborhoods. At $2668, the average rent for a sweet two-bedroom apartment in Boston is the 4th highest in the US. And the energy bill of $287.63 is close to $100 more than would be in Anchorage.

5. Alaska

A newcomer to this list, Alaska – the moose state – offers unsurpassed natural beauty and close-knit culture you’ll never find elsewhere. With only 760 farms, it’s no surprise that most produce and food items are hauled from different states. And that trickles down to tons of other costs. A loaf of bread which goes for a mere $1.79 in Iowa will set you back $4.68 in Anchorage. But again, this is Alaska – the land of amazing wildlife. Paying utility bills ($201.39 for energy) and healthcare isn’t a walk in the park either.

Least Expensive States

1. MississippiOne of the less densely populated states, Mississippi is one of the least expensive states to live in. With low per capita income, the state’s housing costs remain correspondingly low as well (the average home price of $199,028), making the cost of living affordable. Mississippi previously relied mainly on cotton production to drive the economy. In the last two decades or so, however, Mississippi has diversified agricultural and livestock industries, ensuring economic growth. Now focusing on producing rice, soybeans, chicken, and catfish, Mississippi continues to pursue diversification to enrich its economy, a strategy which has been successful so far.

2. Indiana

Next up, is Indiana, a state famous for the Indianapolis 500 and low-cost homes (averaged at $270,204). At the Crossroads of America, you can expect rock-bottom prices for groceries and other basic food items. A head of lettuce goes for a paltry $1.04 while a pound of coffee and ground beef will set you back just $4.43 and $3.74 respectively. A boom in the local economy has pushed prices up a teensy bit, but you can still pick up a check at dinner.

3. Michigan

The Great Lakes State, much like Mississippi and Arkansas, offer low-cost housing (averaged at $274,355) for consumers, yet it’s consistently ranked in the top ten for best states to do business. After all, this is the home of the American auto industry. The average gas price in Detroit was about $2.04 when it hit more than $3 in most parts of the country. The auto industry has bounced back, healthcare is thriving and high-tech jobs are supplanting manufacturing, helping this state become more competitive to prospective employers, keeping the economy working for Michigan citizens.

4. Arkansas

Like Mississippi, Arkansas is a more rural state, offering consumers low housing costs. Arkansas also boasts incredibly low costs for doing business, attracting six Fortune 500 companies to the state. Rent for a two-bedroom apartment is just $700 a month and the monthly energy bill is $145.79, roughly half of what you’d pay in Massachusetts. In short, Arkansas’ low cost of living is balanced by a lower household income than average but still remains a top state for the economic climate.

5. Oklahoma

Rounding up our list is the Sooner State, the home of undulating wheat fields. And the cost of groceries, including a loaf of wheat bread for less than $3, is appropriately cheap. Well, that isn’t all – a grand 2,400 square-foot home will only chip off around $300K from your bank account. With a sub-$150 monthly energy bill and low-cost health care, Oklahoma is certainly one of the best places you’d be lucky to call home.