When you're on your couch looking at rich celebrities online, everything about their lives seem so glamorous and perfect. For every event they attend, they get pampered by six or seven set of hands, and often even have an outfit already tailored for them and ready to go. Although we all wish those red carpet moments really portrayed how the rich dress and look on a daily basis, it's not always the case. If we switch our attention from celebrities for a second and look at the other rich, those who don't spend all their time in front of the camera, we'll notice a drastic difference in wardrobe. Not only do the really rich stay modest with their wardrobe choices, but most of them even dress poorly.

The question is why?

A blog post written for PLRPLR states that "Millionaires are just a different lot of people. They think different. They act different. They spend different. They are different." The author of the article talks about how his uncle was one of the richest men in Virginia but always dressed like he only had a few bucks to spend per month on clothing. In the article, the author mentions how his uncle dressed so poorly sometimes that you might have thought his washing machine was broken or that he worked in the field due to his extremely muddy boots.

The media's depiction of celebrities is all wrong. The rich and famous don't dress in $1,000 suits or dresses, according to the author, because they're smarter than that. Why spend thousands of dollars on pieces of clothing that will wash out, wear down, get lost, or get ripped when you can save the money to invest in real estate or open a business?

That's how the rich think. They prefer to look at efficiency rather than immediate satisfaction. Sure, a $1,000 suit would look amazing and sleek, but you could get a simple tuxedo for about $100 that would also do the job perfectly. As long as the piece of clothing isn't torn and still follows business etiquette, why spend thousands of dollars just for a designer brand or shinier fabric?

They prefer to look at efficiency rather than immediate satisfaction. Sure, a $1,000 suit would look amazing and sleek, but you could get a simple tuxedo for about $100 that would also do the job perfectly. As long as the piece of clothing isn't torn and still follows business etiquette, why spend thousands of dollars just for a designer brand or shinier fabric?

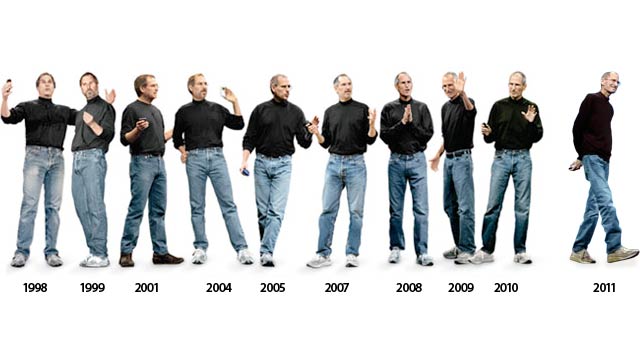

On an episode of Modern Family from earlier this year, there was a story about how Jay, the wealthy grandfather, wasn't fashionable. His young, hot wife was always dressing up and putting on makeup, while Jay always wore sweatpants or nerdy glasses. He was extremely wealthy, yes, but he didn't care about how he looked. As long as he had clothes on, anything went. He preferred comfort and necessity over shiny new clothing or bling.

When you are rich, you are confident enough in your potential and knowledge that you don't feel the need to show off anymore. You know that you have the money and your business shows that you have great earnings, so there's no need to show off the bling. When you're rich, you have a different mentality, one that doesn't revolve around money anymore. You prefer to focus on growing as a person and growing your business instead of debating whether or not you've already worn a certain outfit this week.

There is a famous quote from a very smart person that has always stuck with me, and it goes like this:

"The rich stay rich by living below their means."

All in all, if you follow what the real rich and famous do, you'll be a millionaire too. Spending money lavishly just to show off your earnings isn't going to keep you rich. They might be old values, but it seems to be working for the rich, so why not try it out?

What do you have to lose? Certainly not money.

The question is why?

A blog post written for PLRPLR states that "Millionaires are just a different lot of people. They think different. They act different. They spend different. They are different." The author of the article talks about how his uncle was one of the richest men in Virginia but always dressed like he only had a few bucks to spend per month on clothing. In the article, the author mentions how his uncle dressed so poorly sometimes that you might have thought his washing machine was broken or that he worked in the field due to his extremely muddy boots.

The media's depiction of celebrities is all wrong. The rich and famous don't dress in $1,000 suits or dresses, according to the author, because they're smarter than that. Why spend thousands of dollars on pieces of clothing that will wash out, wear down, get lost, or get ripped when you can save the money to invest in real estate or open a business?

That's how the rich think.

They prefer to look at efficiency rather than immediate satisfaction. Sure, a $1,000 suit would look amazing and sleek, but you could get a simple tuxedo for about $100 that would also do the job perfectly. As long as the piece of clothing isn't torn and still follows business etiquette, why spend thousands of dollars just for a designer brand or shinier fabric?On an episode of Modern Family from earlier this year, there was a story about how Jay, the wealthy grandfather, wasn't fashionable. His young, hot wife was always dressing up and putting on makeup, while Jay always wore sweatpants or nerdy glasses. He was extremely wealthy, yes, but he didn't care about how he looked. As long as he had clothes on, anything went. He preferred comfort and necessity over shiny new clothing or bling.

When you are rich, you are confident enough in your potential and knowledge that you don't feel the need to show off anymore. You know that you have the money and your business shows that you have great earnings, so there's no need to show off the bling. When you're rich, you have a different mentality, one that doesn't revolve around money anymore. You prefer to focus on growing as a person and growing your business instead of debating whether or not you've already worn a certain outfit this week.

There is a famous quote from a very smart person that has always stuck with me, and it goes like this:

"The rich stay rich by living below their means."

All in all, if you follow what the real rich and famous do, you'll be a millionaire too. Spending money lavishly just to show off your earnings isn't going to keep you rich. They might be old values, but it seems to be working for the rich, so why not try it out?

What do you have to lose? Certainly not money.